Did you know?

In 2021, a New Jersey law firm uncovered a $380,000 shortfall in its trust accounts during a routine audit[1]. The audit revealed negative balances and years of mismanaged funds—an oversight that ultimately led to serious repercussions.

Could you ever imagine discovering such a massive gap in your trust accounts? Sounds too unreal, right? Well, trust accounting errors like this happen more often than you might think, and they can happen to any law firm, regardless of size.

These mistakes can be costly, and they often go unnoticed until it’s too late. They quietly accumulate, often emerging only when it’s too late to prevent the damage. In fact, trust accounting errors are one of the primary causes of disciplinary action in law firms. Even minor missteps can escalate into severe financial and reputational harm.

Managing client funds, reconciling IOLTA accounts, and ensuring compliance with complex ethical standards is a high-stakes responsibility. And without precise systems in place, these challenges can quickly turn into liabilities that put your practice at risk.

In this blog, we’ll walk through common pain points of trust accounting and share practical solutions to keep your practice compliant, organized, and protected.

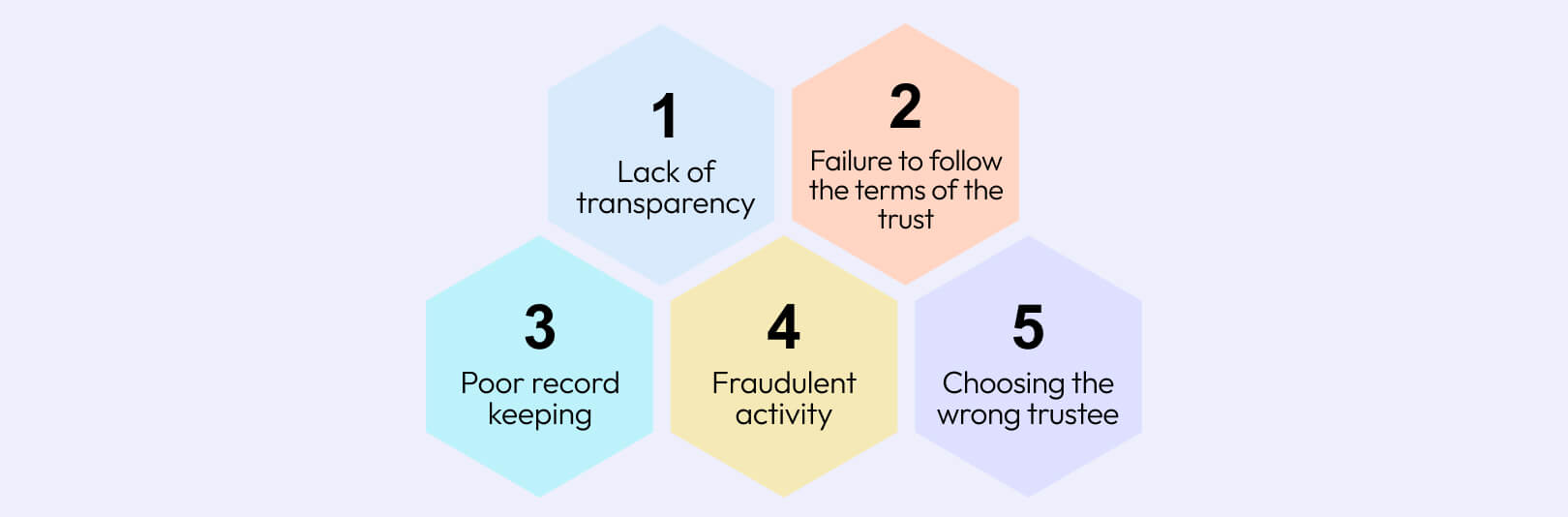

1. Losing track of IOLTA transactions

Managing IOLTA (Interest on Lawyers Trust Accounts) carefully is highly important for law firms. With strict regulatory requirements surrounding IOLTA, firms must meticulously track every transaction to ensure client funds are appropriately managed and accounted for.

Inadequate documentation or maintenance of necessary records can lead to compliance violations, potential audits, and even disciplinary action by state bar associations[2].

How do I handle IOLTA accounts?

A frequent challenge arises when law firms fail to maintain comprehensive backup documentation for each IOLTA transaction. This includes checks, deposit slips, and client disbursement records, all of which must be retained to satisfy ethical obligations.

Documenting each IOLTA transaction would make it easier to substantiate how client funds were handled in the event of an inquiry or audit.

Also read: Top 6 mistakes to avoid in bookkeeping for lawyers

2. Confusing client costs and company expenses

Managing advanced client costs is a critical aspect of law firm bookkeeping that requires precision and expertise. These costs, often incurred as part of litigation—such as filing fees, travel expenses, and expert witness fees—are essentially “mini loans” extended to clients, not income for the firm.

One of the most common mistakes law firms make is categorizing advanced client costs as regular expenses. This can lead to a serious misrepresentation of the firm’s financial status, resulting in inflated profits and potentially higher tax liabilities.

Moreover, misclassifying these costs can cause confusion and financial headaches, especially when reimbursements are expected from clients but aren’t properly tracked.

Advanced client costs should be accounted for as a separate entity—distinct from the firm’s income and expenses. This ensures clear financial reporting and compliance with IRS guidelines. Bookkeepers with specialized expertise in legal accounting can streamline this process, avoiding costly errors.

With dedicated asset accounts and using bookkeeping software like QuickBooks, law firms can manage these costs efficiently, ensuring they are recorded correctly, and ultimately reimbursed without financial discrepancies.

Also read: Top 6 mistakes to avoid in bookkeeping for lawyers

3. Using accounting software with limitations

While tools like QuickBooks and Xero offer general accounting solutions, they are not always sufficient for managing trust accounts in law firms. Many firms rely on these platforms or even Excel income statements, but without legal-specific bookkeeping expertise, errors in trust account management can occur.

These tools might handle basic financials, but trust accounting requires more precision due to stringent regulations. The Thomas Girardi incident[3] is a stark reminder of the risks that can arise from mismanagement.

Missing a new trust accounting rule or failing to reconcile accounts properly can lead to serious consequences, including holds on checks and potential legal violations.

To avoid these issues, law firms should entrust their bookkeeping to professionals who specialize in legal accounting. These experts understand the unique challenges of handling trust accounts and ensure compliance with the latest rules. While technology can streamline processes, it cannot replace the need for dedicated expertise in managing law firm financials.

4. Lack of detailed recordkeeping

Accurate and thorough recordkeeping is essential for managing trust accounts responsibly. Each deposit, withdrawal, and check issued must be carefully documented, immediately recorded, and linked to the correct client account. This level of detail ensures compliance and helps avoid critical errors, like misallocating funds to the wrong client account.

If an audit discovers gaps in documentation, missing transaction records, or misclassified funds, it could trigger compliance issues and lead to disciplinary action by your state bar association. The funds in trust accounts belong to clients, and any mismanagement can quickly escalate from an oversight to a breach of trust, risking fines and even potential disbarment.

An audit trail for every trust transaction, apart from being an ethical responsibility, is also a proactive measure to safeguard your practice from costly mistakes, compliance issues, and reputational damage.

5. Overlooking three-way reconciliation

Despite its importance, three-way reconciliation often gets overlooked by law firms, creating discrepancies that can lead to compliance issues. This monthly reconciliation process ensures accuracy across three essential elements:

- Trust bank account statement

- Trust ledger

- Client ledgers

Here’s how it works: First, reconcile your trust account balance with your trust ledger—similar to balancing a personal checkbook. Then, verify that the sum of all client ledgers matches the reconciled trust ledger balance. If any balances don’t align, it’s likely due to a missing or misentered transaction.

Conducting three-way reconciliation every month, right after receiving your bank statement, keeps your client funds secure and compliant. Skipping this step may seem minor, but unresolved discrepancies can build up and potentially jeopardize your practice’s financial integrity.

Also read: Bookkeeping for lawyers: accounting terms you need to know

6. Mismanaging funds by borrowing from trust accounts

There’s no legal or ethical basis for borrowing from a client’s trust account. Any withdrawal of client funds for personal reasons or to resolve a firm’s cash flow issue is a violation of trust accounting rules and can result in severe disciplinary action, including disbarment.

The responsibility lies squarely with the attorney, even if an office manager, associate, or paralegal initiates the withdrawal. Repayment intentions won’t factor into the judgment when funds have been misused.

For example, in the case of In re: Disciplinary Proceeding Against James Holcomb in Washington State[4], an attorney’s repeated borrowing from a client’s trust account—even with the intention to repay—resulted in disciplinary action. Holcomb took 24 interest-free loans from his client’s trust without advising the client to seek independent counsel or providing transparent documentation. This violation of trust responsibilities led to his suspension from practice for six months.

Borrowing from client trust accounts isn’t just risky—it undermines client confidence and jeopardizes your firm’s credibility. Ensuring trust funds are untouched for any purpose other than their intended use is essential to safeguarding both your reputation and your legal practice.

The bottom Line

Managing trust accounts is one of the most challenging aspects of law firm bookkeeping. The detail required makes it easy to miss small errors that can lead to big consequences. But let’s be honest—you didn’t become a lawyer to spend your time worrying about bookkeeping complexities or compliance hurdles.

That’s where CoCountant steps in.

At CoCountant, we specialize in bookkeeping for law firms, ensuring that every transaction is accurately categorized, every regulation is met, and every client fund is handled with the utmost care. We understand the requirements and pain points of trust accounting and help you avoid common pitfalls like commingling funds, overlooked compliance updates, and misclassified transactions.

With CoCountant, your practice stays protected from financial and regulatory risks, giving you the confidence to focus on advocating for your clients and growing your firm.